Author: Dave Beattie

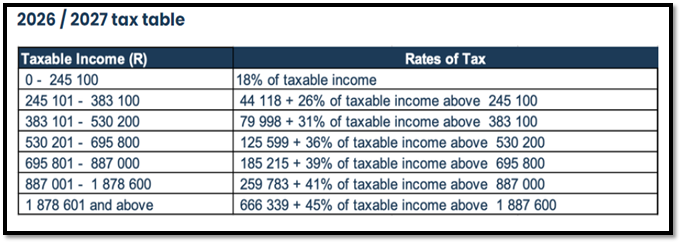

Personal income tax brackets and relief

The personal income tax brackets and rebates have been adjusted for inflation for the 2026 / 2027 tax year (effective 1 March 2026).

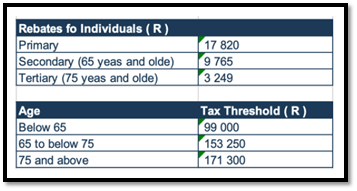

Tax rebates and thresholds

Reimbursive travel rate

No tax payable on reimbursive travel allowances up to R4.95 per kilometre, regardless of vehicle value.

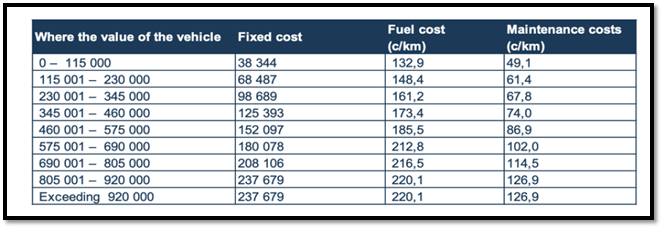

Travel allowance

Updated SARS per-kilometre cost table applies for 2026/27 (vehicle value bands adjusted accordingly).

Medical Aid tax credits

Medical Aid tax credits received an inflationary increase:

- R376 for each of the first two dependants covered

- R254 for every additional dependant

Subsistence allowance

A slight inflationary increase:

- Meals and incidental costs – an amount of R595 per day is deemed to have been expended

- Incidental costs only – an amount of R184 per day is deemed to have been expended

Bursaries and scholarships

The annual remuneration threshold for tax exempt bursaries and scholarships has increased from R600 000 to R900 000.

The updated annual exemption limits for employee relatives are as follows:

- Grade R to Grade 12 (NQF level 1-4) increases from R20 000 to R30 000

- NQF Level 5-10 increases from R60 000 to R90 000

- Disabled employee relatives (Grade R to 12 and NQF Level 1-4) – increases from R30 000 to R45 000

- Disabled employee relatives (NQF Level 5-10) increases from R90 000 to R130 000

Long Service / Bravery awards

The exemption relating to awards for bravery and long service increase from R5 000 to R16 000.

Employee loans for immovable property

The qualifying property value for employer-provided loans used to purchase immovable property has been increased from R450 000 to R650 000.

The associated remuneration threshold linked to these property acquisition loans has risen from R250 000 to R360 000.

Compensation exemption – death in the course of employment

The tax-exempt amount payable to an employee’s beneficiaries when death occurs as a result of, and during, the course of employment has been increased from R300 000 to R800 000.

Retirement Fund contributions

The previous limit of R350 000 was increased to R430 000 for being the maximum now allowed. This is a welcome adjustment for those taxpayers who want to put more money away for retirement and maximise the tax benefit.

Accommodation benefit formula

The threshold used to calculate the taxable value of residential accommodation has increased from R95 750 to R99 000.

Capital Gains tax amendments

The annual CGT exclusion increases from R40 000 to R50 000.

The exclusion in the year of death rises from R300 000 to R440 000.

The disposal of primary residence exclusion increases from R2 million to R3 million, with the same R3 million threshold applying where the proceeds from the sale of the primary residence do not exceed this amount.

Tax-free investments

The annual threshold of investments in tax-free investment financial instruments or policies by individuals has increased from R36 000 to R46 000.

Value-added Tax (VAT) adjustments

The VAT rate remains unchanged at 15%.

The VAT compulsory registration threshold has increased from R1 million to R2.3 million per annum.