|

| Editor's Note |

With continued pressure on the economy, over the coming months we are going to be looking in more detail at relevant issues impacting retrenchments and change management. In this edition, we look at whether one can one force changes in employment conditions in reaction to changing economic or customer conditions. We also remind readers of the small number of individual tax payers propping up our tax base and the risk this creates for the fiscus.

On a more positive note we look at the benefits of having a coach as a small or medium business leader and provide practical tips for buying a business.

Finally, we include a short article on the leave implications for commission based employees.

As usual, should you require any further detail on any of these topics, please feel free to contact us.

Personal tax filing season starts on the 1 July. If you would like our help preparing your return, please read the relevant section of this newsletter explaining how much it will cost and what you need to do.

We do offer a referral scheme for new clients sent in our direction so if you know of anyone looking for outsourced payroll services then please let us know*.

*Terms and conditions apply |

| Top of Page |

| |

| Table of Contents |

1. How many individual tax payers prop up South Africa's tax base?

2. What are the leave implications for employees on commission?

3. Important Things to Think About when Buying a Business

4. Why do you need a coach?

5. Forced Changes to Conditions of Employment

6. Personal Tax Filing Season Starts 1 July

7. Contact HRTorQue |

| Top of Page |

| |

| 1. How many individual tax payers prop up South Africa's tax base? |

| Source: Payroll Authors Group |

Editor's Note: while the stats below make for interesting reading the bigger concern is how fragile the South Africa tax base really is and how little room the Minister of Finance has to manoeuvre.

For the 2017 tax year, Personal Income Tax (PIT) is forecast to contribute 37,5% to the total tax revenue that runs our country, with VAT next in line at 25,6% followed by corporate income tax at 16,9%.

The grouping of PIT taxpayers always makes for interesting reading. Consolidation of the budget's estimates for 2016/17 of the number of individual taxpayers and their income tax paid shows that:

1. 6% of taxpayers pay 47% of the total R441 billion PIT revenue; or

2. 429 173 individual taxpayers pay R207 billion of the total R441 billion PIT revenue

The 47% contribution by the 6% high income taxpayers means that their PIT is about 18% of the total tax revenue of R1 175 billion that runs South Africa. There are only just over 400 000 of them.

While we can breathe a collective sigh of relief that employees escaped an increase in the top marginal PIT tax rate of 41% for 2016/17, bear in mind that the Minister of Finance made it clear that under current financial circumstances taxes will have to be raised to increase tax revenue by about R15bn per year for the next two years.

If the situation doesn't improve before then, individual taxpayers will probably need to contribute through increased marginal tax rates. |

| Top of Page |

| |

| 2. What are the leave implications for employees on commission? |

| Author: Karen van den Bergh |

Commission based employees would be entitled to the same amount of leave as any other employee.

• Annual Leave of 21 consecutive days (15 working days for a five day worker).

• Sick Leave of 30 days in a three-year cycle.

• Family Responsibility leave of 3 days per annum.

In terms of calculating payment for these days you would need to take the preceding 13 weeks of earnings or a representative 13 weeks and average it to calculate the daily rate. |

| Top of Page |

| |

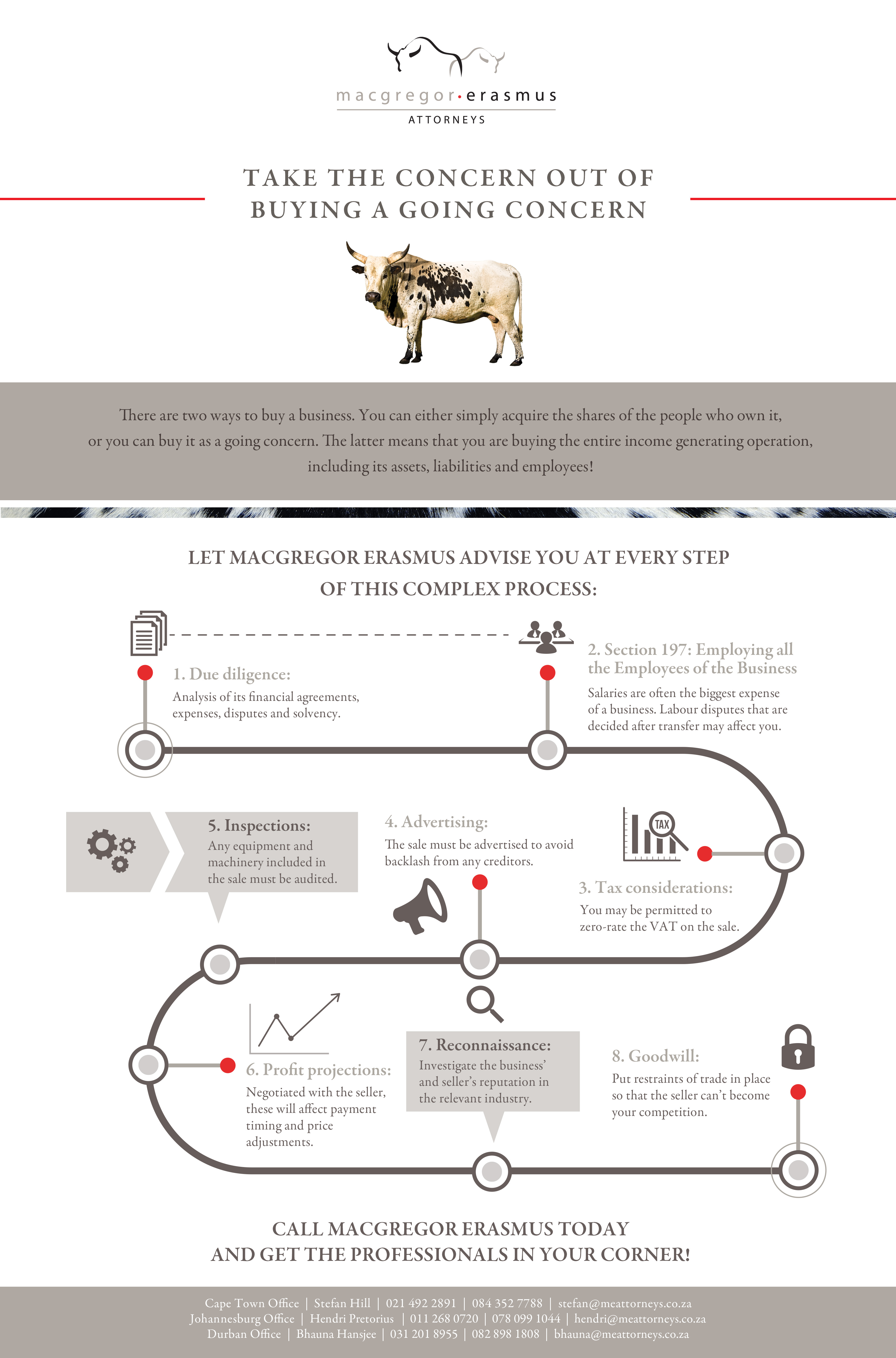

| 3. Important Things to Think About when Buying a Business |

| Author: MacGregor Erasmus Attorneys (www.meattorneys.co.za) |

Many of our clients come to see for assistance when they are buying a new business. What they don't realise is that there are two ways to do it. Either as a going concern (asset purchase) or by buying the shares / members' interest of the person or people that own and operate the business. This decision alone can make a difference to the level of risk and chances of success.

In addition to making the right choice on how to buy the business below are some of the top tips to avoid other common and costly errors:

1. Conduct a full financial and legal due diligence of the business venture you are interested in to identify key value issues including (amongst others):

• Financial agreements the business venture is tied in to;

• Total monthly expenses to creditors, including employees;

• Labour disputes that may still be pending or subject to further action such as reviews;

• Company solvency with verifiable financial statements

2. Speak to your tax advisor about whether the sale can be zero-rated

Buying as a going concern often permits you to zero-rate the VAT on the sale.

3. Advertise the sale in terms of the Insolvency Act

The sale must be advertised prior to the effective date to avoid creditors attacking the disposition by the sellers and trying to set it aside as void. This is something you should be checking during your due diligence regarding outstanding creditors' claims.

4. Equipment reliant business

If the business is in manufacturing/plant or heavily reliant on equipment, you must inspect and audit all machinery and itemise each and every component that forms part of the sale and provide for an inspection prior to taking transfer. You need to also be sure the equipment is not outdated, faulty or unnecessary. The value of the equipment is part of the purchase price and you need to ensure that on transfer of the business you have working machinery to continue production.

5. Profit projections

If you are worried about the business under new management, consider agreeing a projection from the seller based on historic progress and realistic figures to form part of the agreement and if possible, stagger payment of the purchase price to accommodate any adjustments if the seller's representation was way off the mark and you over paid. This will have to be drafted to ensure that it takes market and unforeseen circumstances into account.

6. Protecting the goodwill after the sale

A business may be successful and profitable because of the relationships that the seller/s have built up over time. The seller is receiving value from you in terms of the purchase price for you to acquire that profitability. It is imperative that you protect your acquisition by ensuring that the seller/s does not start up in competition with you and use their relationships and success to unfairly compete with you. You must put adequate and enforceable restraints of trade and confidentiality undertakings in place to protect your investment and the goodwill of the business that you are purchasing.

Please download our infographic: "Buying a Going Concern". |

| Top of Page |

| |

| 4. Why do you need a coach? |

| Author: Iole Matthews |

In the pressurised and action orientated world of small and medium sized business, a coach might well be the ultimate secret weapon in maximising your potential.

While the corporate world has long used coaches to support and develop executives, smaller businesses that face similar challenges have rarely had access to this type of support. Without all the resources of big business, entrepreneurs in medium and small businesses often feel isolated and short of support as they deal with day to day issues. They also often face additional pressure as they play multiple roles, which might include managing staff, planning strategy, monitoring production, customer service and finding new markets, the list is endless.

In this pressured environment, trying to find time for full day training workshops and seminars means that personal development goes way down the wish list and becomes a "nice to have" rather than an integrated part of business operations. This is where coaching can provide an efficient and effective solution for achieving personal and professional excellence.

So what is coaching? Essentially coaching is a focused and co-operative partnership with someone whose only agenda is your agenda. A coach works with you to identify where you are now, defines where you want to be and then supports you in getting there in the most effective way. Sessions are scheduled every three to four weeks and run for approximately an hour, with additional support provided via telephone, or even Skype. A coach can act as a sounding board in thinking through important decisions, can help with accountability around action plans and build momentum by helping you take responsibility for results and outcomes.

An investment in business coaching pays for itself, increasing the bottom line, getting more done by working smarter, helping you work with renewed passion and finding ways to reclaim your life by improving your work-life balance.

However, before you consider coaching, ask yourself some key questions:

| 1. |

Am I ready to create and clarify a compelling vision for my life and business? |

| 2. |

Am I ready to take action on that vision? |

| 3. |

Am I open to trying new ideas instead of continuing to do the things that have not worked in the past? |

| 4. |

Am I willing to stop self-defeating behaviours? |

| 5. |

Am I willing to discover and change fears and beliefs that hold me back? |

| 6. |

Am I ready to accept responsibility for my success and happiness in life? |

If you answered yes to these questions then business coaching is for you. |

| Top of Page |

| |

| 5. Forced Changes to Employment Conditions |

| Author: Ivan Israelstam |

An employee is entitled, in terms of Section 77(3) of the Basic Conditions of Employment Act, to ask either the civil courts or the Labour Court to determine any matter concerning a contract of employment. As a contract can be an enforceable even if it is not in writing, the employee can even take a dispute relating to an oral or tacitly agreed contract to these courts. In addition, the employee, if dismissed for refusing to accept changes to his/her employment conditions, can sue the employer for unfair dismissal.

| • |

The above is problematic for employers because their operational circumstances often create the genuine need to change the employment conditions of employees. |

Modern day production pressures lead senior managers to transfer such pressures for change on to line management. Line management in turn attempt to relieve the pressure by trying to force the changes through as quickly as possible. This often results in severe employee relations problems and contraventions of the law. Labour law severely restricts the employer's right to make such changes without the employees' consent.

Specifically, under the Labour Relations Act (LRA):

| • |

It is not a disciplinary offence for an employee to disobey an unreasonable instruction. And it would not normally be unreasonable for an employee to refuse to work according to new terms and conditions unless this has been agreed to by the employee or his/her representative. |

| • |

In a takeover of a going concern the employer is compelled to retain the terms and conditions of employment of the employees concerned. |

| • |

Unfair acts on the part of the employer as regards employee benefits are prohibited. |

| • |

Section 187(1)(c) of the LRA prohibits the employer from firing employees who refuse to agree to changes in terms and conditions of employment. Specifically, this section provides that: |

"A dismissal is automatically unfair if an employer, in dismissing the employee, acts contrary to section 5 or if the reason for the dismissal is... to compel the employee to accept a demand in respect of any matter of mutual interest between the employer and employee...". This applies where the employer threatens the employee that, if he/she does not agree to a change in terms and conditions of employment, the employee will be dismissed. If the employee then refuses to agree to the change and is consequently dismissed this could be seen to be automatically unfair.

However, what if the employer needs to change the work circumstances due to its operational requirements? That is, what if, for example, client work circumstances are such that a new shift system is required but the employees are not willing to agree to the change? Is the employer entitled to go into a retrenchment process with a view to hiring employees willing to accept the new terms and conditions of employment?

In the case of CWIU and others vs Algorax (Pty) Ltd) (2003 11 BLLR 1081) the employer needed to switch to a new shift system but the employees refused to accept this. The employer then retrenched its employees but consistently said that it would re-employ them if they would change their mind and agree to the new shift system.

The Labour Appeal Court found that:

| • |

The retrenchments could have been avoided or minimised if the employer had got rid of a number of contractors. |

| • |

The employer's firm and consistent statements that the employees would be taken back if they agreed to the new shift system showed that the employer had ulterior motives. |

| • |

The dismissals were not genuine retrenchments but were instead a ploy to get the employees to agree to a change in their conditions of employment. |

| • |

The dismissal was therefore automatically unfair in terms of section 187(1)(c). |

| • |

All the employees were to be re-employed with effect from the date of the court order. |

In the case of Pedzinski vs Andisa Securities (Pty) Ltd (2006, 2 BLLR 184) The employer informed the employee that, if she did not agree to extend her working hours to full day she would be retrenched.

When she was retrenched she took the employer to the Labour Court where it was decided that:

| • |

The employee had been threatened with retrenchment in order to coerce her into extending her working hours. |

| • |

Her dismissal was automatically unfair. |

| • |

The employer was to pay the employee compensation equivalent to 24 months remuneration as well as the employee's legal costs. |

While the making of such changes are often justified employers need to be extremely careful as to how they go about this. Therefore, before they begin to implement any changes that affect employees, employers need to get advice from a labour law expert who also understands practical operational needs. |

| Top of Page |

| |

| 6. Personal Tax Filing Season Opens 1 July |

| Author: Dave Beattie |

The tax filing season officially starts on 1 July 2016 for the 2016 tax year (1 March 2015 to 29 February 2016). It is anticipated that the closing date for e-filing submissions will be the end of November 2016 for normal taxpayers and the end of January 2017 for provisional taxpayers.

Pricing

Our charges for completing tax returns will depend on when we receive your information. Premium pricing will kick in for last minute returns to try and avoid the challenges we face every year.

| Information Received By |

Cost (incl. VAT) |

| 15 October 2016 (15 December for provisional taxpayers) |

R700 |

| After 15 October 2016 (later than 15 December for provisional taxpayers) |

R1,000 |

Please note we reserve the right to charge a surcharge on the completion of tax returns that require the drafting of additional schedules.

The cost of completing these tax returns will include the following services:

| • |

Collection and collation of supporting documentation necessary to complete your tax return. |

| • |

Completion and filing of the tax return. |

| • |

Checking of assessment and notifying you of the result thereof. |

| • |

Submitting any additional information requested by SARS via e-Filing. |

Process

Due to the volume of work anticipated during this filing season and the need to maintain the high standards required by the South African Institute of Tax Professionals I will be assisted this year by Bruce Laister. Bruce is a highly qualified tax practitioner in his own right having a BCompt through UNISA and registrations as a tax practitioner with SAIT and SARS.

Returns that are submitted via e-Filing are generally assessed within a couple of minutes and the assessment will be forwarded to you in cases where payments to SARS need to be made. If you are due a refund, please keep an eye on your bank account and notify me if you have not received it within 30 days. Due to the volume of returns submitted it is not possible to monitor the progress of each refund payment. SARS no longer sends out notifications where they experience bank account problems; and due to Call Centre congestion and the risk of fraud they are loathe to assist with refund verifications.

If you have all the necessary documentation to complete your tax return and would like to be one of the 'early birds' please can you get this information through to me as soon as possible and the work will be processed on a first come, first served basis.

Provided you are on my e-Filing profile we will endeavour to lodge your return within 72 hours. For new clients your details will need to be loaded onto my e-Filing profile. Once loaded into e-Filing it takes approximately 48 hours for the profile to be activated. Please note that the information that you provide in this regard must be exactly that which is reflected on e-Filing, otherwise the request will be rejected.

In the event of SARS making an error on the assessment the tax return completion fee includes a maximum of 30 minutes consulting with SARS on your behalf. Any interventions that exceed this period will be billed at an hourly consulting rate of R 650 plus VAT. This approach is necessary due to the ever increasing errors made by SARS. Should you wish to take up the issue personally we will forward you all the necessary supporting documentation to do so.

Once all the information requested above is received the tax return will be prepared to the point where it is ready to be submitted to SARS. An invoice for this service will then either be emailed or posted to you. Kindly make payment as soon as possible and fax the proof of payment, with your name clearly marked on it to 031 564 1228 (marked for the attention of GT). Your tax return will then be lodged via e-Filing. It has unfortunately become necessary to operate in this manner as the Tax Division has recently been saddled with a significant amount of bad debt.

Information requirements

To complete your tax return accurately and timeously we require the following information:

| • |

IRP5 certificate / s (Please request a copy from your employer so that we can verify that the IRP5 agrees to the IRP5 on the pre-populated tax return). |

| • |

IT 3(a)'s relating to untaxed income, IT 3(b)'s for interest and dividends and IT 3(c)'s for any capital gains received. |

| • |

Sale of any capital assets. |

| • |

Details of any other income that you may have received from any sources (e.g. if earning rental income we would need the total income earned in the year and a schedule of the expenses incurred in generating the rental income (i.e. interest paid on bond, levies, management fees, repairs and maintenance, electricity / lights and water etc.). |

| • |

Medical aid tax certificate. |

| • |

Retirement annuity tax certificate. |

| • |

Travel details: opening and closing mileage, business / private km's, total km's travelled, car make and model and original cash purchase price. You are required to maintain a detailed logbook if you want to claim business mileage against your travel allowance. This detail includes the clear separation of the business and private mileage undertaken and the listing of the clients visited daily. Please email this logbook to me. |

| • |

Should you have use of a company car please note that you are required to maintain a detailed logbook. In the event of a SARS review / audit this detailed logbook will need to be sent to them. Please email this logbook to me. |

| • |

If you earn mainly commission (more than 50% of total remuneration) then we require a schedule listing the expenses that you incurred during the tax year to earn that commission. Please retain the supporting documentation for 5 years as SARS may audit you at any time. |

If any of the details listed below have changed please notify me so that we can make the necessary changes on the tax return:

| • |

Marital status (kindly advise if you are married in / out of community of property). If you are married in community of property and receive investment or rental income in addition to your salary please send through your spouse's name and ID number. |

| • |

Residential and postal address. |

| • |

Telephone / cell phone numbers / email address. |

| • |

Bank details: account number / holder, branch code and type of account (very important). If these details change you will be required to take a certified copy of your ID, proof of residence and original current bank statement (with bank stamp on it) to your nearest SARS office in person. SARS requires you to do this in person due to recent occurrences of fraud. |

|

| Top of Page |

| |

| 7. Contact HRTorQue |

Head Office (Durban)

Phone: 031 564 1155 • Email: [email protected] • Website: www.hrtorque.co.za

Address: 163 Umhlanga Rocks Drive, Durban North, KwaZulu-Natal

Johannesburg Office

Ground Floor, West Wing, 6 Kikuyu Road, Sunninghill, 2191 |

|

|

|

|

{kind=link}